Categories

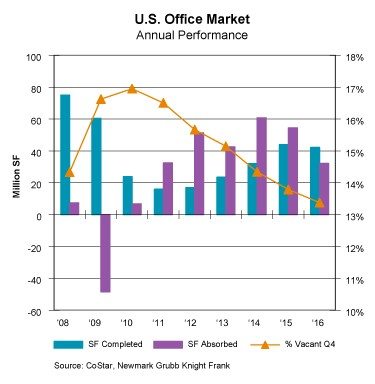

The U.S. office market tightened in 2016 for a sixth consecutive year, although it showed signs of reaching equilibrium as vacancy stabilized in the fourth quarter and deliveries exceeded absorption by a wide margin. Here are the key points:

Outlook Several of the programs touted by the incoming Trump administration—tax cuts, infrastructure spending and lighter regulatory burdens—could stimulate business capex and thereby prolong the economic expansion, which, at 91 months, is already one of the longest since World War II. Nevertheless, with the labor market near full employment, these programs are unlikely to have much effect on the modest pace of hiring. Expect absorption and deliveries of new office space to balance each other out in 2017 and 2018. New buildings will lease up, as will second-generation space left behind by relocating tenants, but at a slower pace. The U.S. vacancy rate is on track to rise by 10 basis points in 2017 and then level out in 2018. Asking rents should continue to rise at a modest pace in the low single digits over the next two years, pushed higher by premium rates in newly delivered projects. Tenant concessions packages are likely to become more generous for available second-generation space. |

Chris Falk is a Certified Commercial Investment Member (CCIM)—one of the most comprehensive commercial real estate designations, held by an estimated 6% of commercial brokers nationally. As a commercial real estate broker, Chris has handled over 600 transactions exceeding $475MM. Born and raised in Utah, Chris understands the unique qualities of the region and the great capacity for business opportunities in Northern Utah, including Davis, Weber and Salt Lake Counties. Chris is the premier, go-to agent for businesses and developers interested in this dynamic area.