Categories

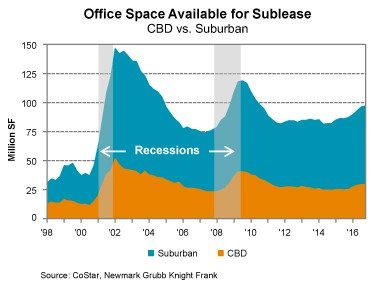

| Office sublease space has been rising gradually, nationwide and here locally in Utah. On a national level, sublease amounts were tallied at the recent low of 81.5 million square feet available at mid-2014 to 97.1 million square feet at year-end 2016. The maturing expansion cycle and local conditions in several key markets are driving this trend. Let’s examine these one at a time:

Absorption of sublease space was strongest early in the expansion cycle, as tenants snapped up the bargains available from the oversupply of space created during the recession. From 2010 to 2012, tenants absorbed a surprisingly strong 4.5 million square feet of space offered for sublease, as they were willing to sign a shorter-term lease in exchange for a low price. Some of these tenants likely welcomed the shorter lease term because the economy remained on shaky ground during the early years of the recovery.

Then absorption turned mildly negative in 2013 and 2014 and more sharply negative in 2015 and 2016. As new construction deliveries escalated during these years, relocating tenants added to the pool of sublease space, while tenants who might have considered sublease earlier in the cycle enjoyed a wider range of options. Adding to the late-cycle increase in available sublease space are local conditions that have pushed sublease totals higher in certain markets, notably Houston, where tenants—primarily oil and gas businesses—drove the sublease availability rate to 5.6%, well above the U.S. average of 2.0%. Other markets with elevated sublease inventories include Northern New Jersey, where downsizings at large corporate headquarters facilities have pushed the sublease availability rate to 3.0%, and Silicon Valley, where tighter funding for tech startups drove sublease availability to 2.8%. Sublease Outlook Opposing forces will play out in the sublease market over the next few years, potentially resulting in a stalemate that will leave sublease levels at about where they are now until the next recession hits, perhaps in 2019. Some tenants relocating to newly completed projects will continue to leave behind pockets of sublease space. Potentially counteracting this slow increase will be the fiscal stimulus proposed by the Trump administration—tax cuts and infrastructure spending—along with relaxed business regulations. These may have a particularly salutary effect on small businesses, as noted by the NFIB Small Business Optimism Index, which is at its highest level since 2004. For some of these smaller or startup companies, a low-priced, limited-term sublease opportunity may be just the ticket. |

Chris Falk is a Certified Commercial Investment Member (CCIM)—one of the most comprehensive commercial real estate designations, held by an estimated 6% of commercial brokers nationally. As a commercial real estate broker, Chris has handled over 600 transactions exceeding $475MM. Born and raised in Utah, Chris understands the unique qualities of the region and the great capacity for business opportunities in Northern Utah, including Davis, Weber and Salt Lake Counties. Chris is the premier, go-to agent for businesses and developers interested in this dynamic area.